The Middle East and Global Energy Markets

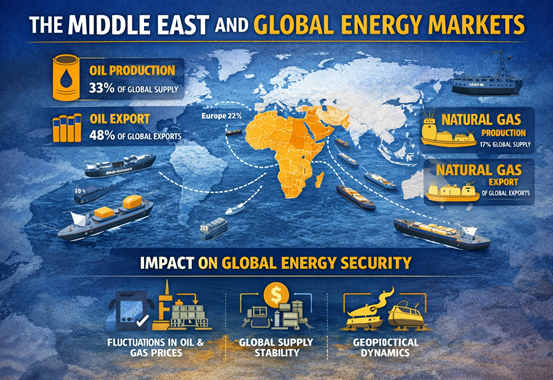

The IEA is closely monitoring the situation in the Middle East, including the potential implications of continued disruptions to energy flows through the Strait of Hormuz. Read the latest statement from IEA Executive Director Fatih Birol. The war in the region that began on 28 February has impeded oil flows through the Strait, with export volumes of crude and refined products currently at less than 10% of pre-conflict levels. This is forcing operators across the Gulf region to shut in or curtail a substantial amount of production. The region’s output of liquefied natural gas (LNG) has also been significantly impacted. The IEA will continue to assess the energy security implications of the situation in coordination with governments around the world. Current market backdrop Oil and natural gas prices have spiked since the start of hostilities. Brent crude futures climbed by 35% through 9 March, and Dutch TTF, the European benchmark for natural gas, was up by 75%. Moreover, some markets for oil products have been particularly affected, including those for diesel and jet fuel. The global oil market was in significant surplus throughout 2025. Ahead of the military actions that began on 28 February, global oil supply was also expected to far exceed demand in 2026. However, prolonged supply disruptions could flip the market into a deficit. As regional storage tanks fill up, producers in Iraq, Kuwait, Qatar, Saudi Arabia and the United Arab Emirates (UAE) have announced cuts to their output. Further curtailments of production may become necessary unless export flows resume. Global observed oil inventories rose to more than 8.2 billion barrels in 2025, their highest level since 2021. These stocks now provide a welcome cushion against supply disruptions. Notably, IEA Member countries hold over 1.2 billion barrels of public emergency oil stocks. These, and a further 600 million barrels of industry stocks held under government obligation, can bring additional supply to market if needed. Natural gas markets had been gradually rebalancing following the major shock that followed Russia’s invasion of Ukraine in February 2022. A wave of new LNG capacity between now and the end of this decade is expected to transform market dynamics. But markets remained tight in the first two months of 2026, and depleted storage coming out of the heating season in the Northern Hemisphere is set to increase the call on LNG in the months ahead. An extended loss of output from the Ras Laffan facility in Qatar could significantly exacerbate this market tightness. Production was shut down following an attack on the facilities on 2 March. In 2025, Ras Laffan produced 112 billion cubic metres (bcm) of LNG, as well as 300 000 barrels per day of liquefied petroleum gas (LPG) and 180 000 barrels per day of condensate, making it the largest LNG facility in the world by some distance. The Gulf region is a key source of exports of refined oil products to global markets, notably for middle distillates such as diesel and jet fuel. Globally, markets for middle distillates have been relatively tight compared with those for other products, driven in part by sustained imports into European markets. As such, there appears to be little flexibility for refineries outside the region to increase the yield of diesel and jet fuel further to compensate in the event of sustained supply losses. Additionally, the Middle East is a major source of other products derived from oil, including liquefied petroleum gas (LPG) and petrochemical feedstocks. Numerous refineries and downstream assets that produce these products have been impacted by the conflict. Strait of Hormuz: Key facts The Strait of Hormuz is a narrow sea passage, separating the Arabian Peninsula and Iran, and connecting the Persian Gulf with the Gulf of Oman and the Arabian Sea. A crucial trade artery, it is the primary export route for oil and natural gas produced by Saudi Arabia, the UAE, Kuwait, Qatar, Iraq, Bahrain and Iran. An average of 20 million barrels per day (mb/d) of crude oil and oil products transited the Strait of Hormuz in 2025, or around 25% of the world’s seaborne oil trade. Oil and LNG markets would face significant supply disruptions if shipping through the Strait is interrupted for an extended period. Options for oil flows to bypass the Strait of Hormuz are limited. Only Saudi Arabia and the UAE have operational crude pipelines that could potentially reroute flows to bypass the Strait, with an estimated 3.5 mb/d to 5.5 mb/d of available capacity. Other countries, including Iran, Iraq, Kuwait, Qatar and Bahrain, rely on the Strait to deliver the vast majority of their oil exports. Oil products transiting the strait of Hormuz by destination, 2025 About 80% of oil and oil products transiting the Strait in 2025 was destined for Asia. However, shipping disruptions are having a global impact on oil prices. In addition, over 110 billion cubic metres (bcm) of LNG passed through the Strait of Hormuz in 2025. About 93% of Qatar’s and 96% of the UAE’s LNG exports transited through the Strait, representing almost one-fifth of global LNG trade. There are no alternative routes to bring these volumes to market. Most LNG from Qatar and the UAE goes to Asia. In 2025, almost 90% of the total volumes exported via the Strait of Hormuz was destined for the Asian market. Just over 10% went to Europe. Impact on other key commodities Various other commodities markets have also been affected by disruptions to shipping in the Strait of Hormuz, with implications for energy and beyond. Fertiliser supply is particularly exposed. More than 30% of global trade of urea moves through the Strait, along with about 20% of trade of ammonia and phosphate. This creates risks for food prices and security. Moreover, disruptions in this sector could have indirect effects on energy markets, since some countries use imported LNG to run domestic fertiliser plants. Additionally, the Gulf region produces around 8% of the global supply of aluminium, which is used in numerous energy technologies, as well as in construction and manufacturing. About 5 million tonnes of the metal are shipped each year through the Strait from smelters in Bahrain, Qatar, Saudi Arabia and the United Arab Emirates. Around half of global seaborne sulphur trade also moves through the Strait of Hormuz. Sulphuric acid is used not only to produce fertiliser and chemicals, but also in the refining of petroleum and critical minerals such as copper, nickel and zinc. Source: International Energy Agency (IEA) Energy prices fall and stocks rise after Trump says Iran war 'very complete' Oil prices fell sharply on Tuesday after US President Donald Trump said that the war in Iran would come to an end "very soon". Crude had reached almost $120 a barrel on Monday over fears that the conflict would cause lengthy disruption to energy supplies from the Middle East, but dropped back to around $90 following Trump's comments. Although oil prices are still significantly higher than they were before the war, European stock markets rebounded with London's FTSE 100 index rising 1.9%. Gas prices also receded. Trump said he thought "the war is very complete, pretty much", although he later warned Iran to not block the Strait of Hormuz, a shipping route crucial to global energy supplies. Source: British Broadcasting Corporation (BBC) Tuesday 10th March, 2026